What's Typically Covered: Sudden, Accidental Water Damage

Standard homeowners insurance in Texas typically covers sudden, accidental water damage, including a burst pipe, toilet overflow, or appliance failure like a washing machine or water heater malfunction. The key word is sudden. A pipe that fails without warning is a different situation under most policies than damage that built up gradually.

Insurers generally look at the cause of loss first, not just the visible damage. A pipe that bursts because of a sudden freeze event is treated differently than a pipe that's been slowly weeping behind a wall for months, even though both eventually produce similar-looking water damage on the surface.

What's Typically Excluded: Gradual Leaks and Rising Floodwater

Gradual leaks and seepage are usually excluded, since insurers expect homeowners to catch and fix slow leaks before they cause significant damage. Rising floodwater, including overflow from Big Fossil Creek or any of Haltom City's other named creeks, also typically requires a separate NFIP or private flood policy, since standard homeowners insurance generally excludes it. Mold remediation beyond a policy cap, often in the $1,000 to $5,000 range depending on the policy, is another common exclusion.

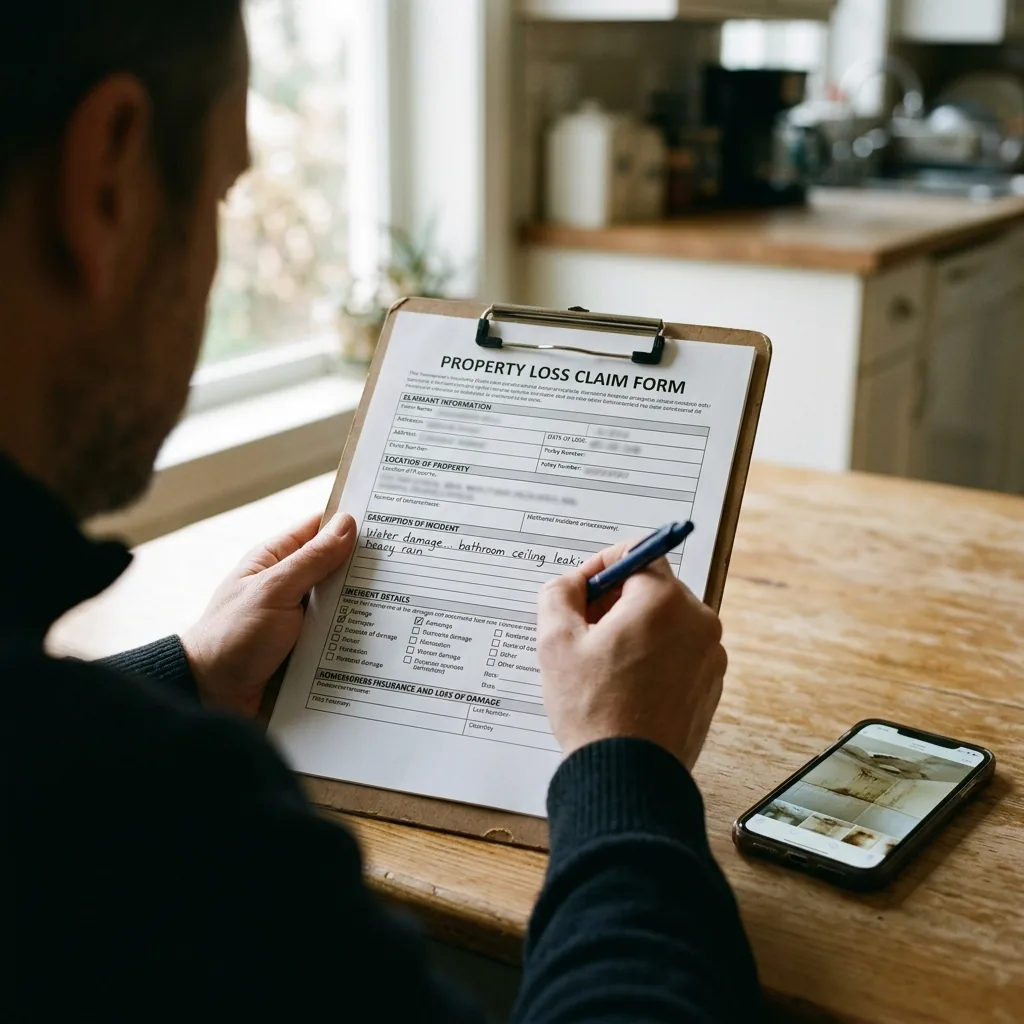

This is part of why documentation matters so much. An adjuster reviewing a claim is often trying to determine which category a loss falls into, and the homeowner's own photos and timeline can be the deciding factor in a borderline case.

Texas's Claim Timeline Requirements

Texas Insurance Code Chapter 542 sets clear deadlines for insurers handling a claim. An insurer must acknowledge your claim within 15 business days, and accept or deny it within 15 business days of receiving a completed proof of loss. Once a claim is accepted, the insurer has 5 business days to pay. These aren't suggestions. They're statutory deadlines your insurer is required to meet.

If your insurer misses one of these deadlines, that's worth raising directly with them or with the Texas Department of Insurance. Knowing the actual statutory timeline gives you a concrete benchmark instead of just waiting and hoping the claim moves along.

How We Document Your Claim

We document every step of a water damage job with moisture readings, drying logs, and photos your adjuster can use, regardless of which way your specific claim is likely to go. A clean, complete paper trail makes the difference between a claim that moves smoothly and one that gets delayed over disputed details.

That documentation includes the original moisture map showing the full extent of the damage, daily readings as drying progresses, and a final report confirming the structure met IICRC S500 drying standards before we considered the job complete.

We respond across all Haltom City neighborhoods, 24/7. If you're dealing with water damage right now, our emergency water damage restoration team can get started immediately and handle the documentation your claim needs. Call (817) 973-0943. A live dispatcher answers every call.